SMM, February 8:

As of January 27, the most-traded SHFE zinc contract closed at 23,655 yuan/mt, down 1,805 yuan/mt in a single month, a decline of 7.09%. Zinc prices fell throughout January, reaching a high of 25,305 yuan/mt at the beginning of the month and a low of 23,470 yuan/mt at month-end. Zinc prices showed a significant decline overall in January. Will they rebound in February?

From a macro perspective, at the beginning of January, the US reported high inflation rates, leading the market to expect the US Fed might slow down its pace of interest rate cuts. Subsequently, with Trump taking office, the market began to price in some related political and economic policies. The US dollar index fluctuated at highs, and bearish funds entered the market, putting pressure on zinc prices. Moving into February, the US implemented tariffs on China and Canada, escalating trade tensions and further weighing on zinc prices. Continued attention is needed on subsequent overseas macroeconomic developments.

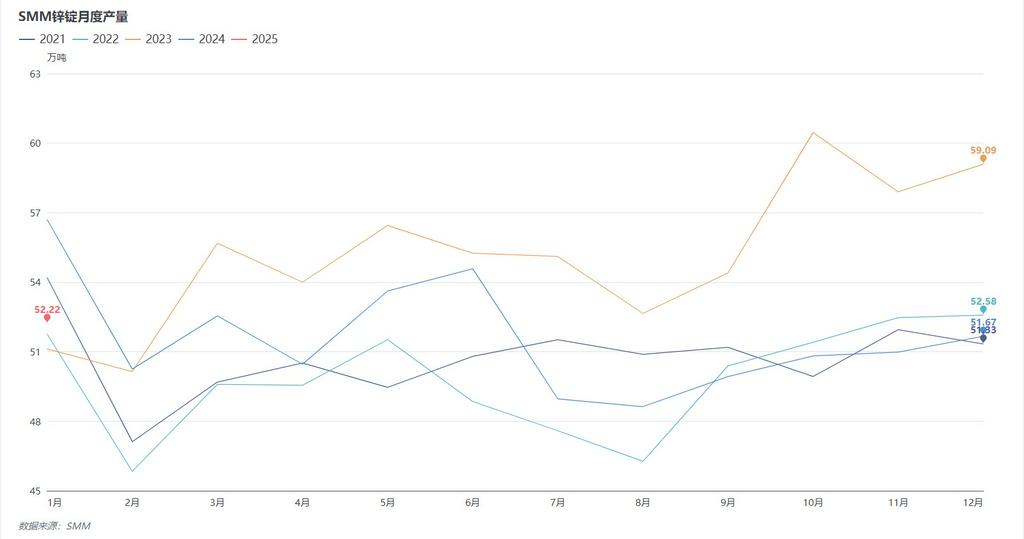

On the supply side, China's refined zinc production in January increased by 5,500 mt MoM, with a limited overall growth rate. Coupled with the limited opening time of the zinc ingot import window in January, the inflow of imported zinc ingots remained stable, and overall zinc ingot supply did not show a significant increase. Entering February, due to the impact of the Chinese New Year holiday and insufficient production days, domestic refined zinc production is expected to decline, and zinc ingot supply may weaken significantly.

On the consumption side, as the Chinese New Year holiday approached, domestic downstream zinc enterprises gradually began to suspend production, with holiday durations ranging from a few days to several weeks. Most downstream enterprises had insufficient production days in January. Although some enterprises stocked up on zinc ingots before the holiday, overall zinc ingot consumption still declined significantly. Entering February, most downstream zinc enterprises are not expected to fully resume production until after the Lantern Festival. The Chinese New Year holiday will also impact enterprise operations in February, and domestic downstream zinc consumption is expected to recover only to a limited extent.

Overall, zinc ingot supply growth was limited in January, while downstream demand weakened significantly, providing insufficient support for zinc prices. Additionally, the domestic zinc ore market gradually loosened, causing zinc prices to decline throughout January. Looking ahead to February, as downstream enterprises gradually resume production, attention should be paid to the recovery of consumption and changes in the macroeconomic environment.

For SMM lead and zinc industry data packages, please contact: Penghui Tang

Phone: 15008461791